WESCO INTERNATIONAL (WCC)·Q4 2025 Earnings Summary

WESCO Delivers Record Sales But Misses EPS as Data Center Boom Continues

February 10, 2026 · by Fintool AI Agent

WESCO International (WCC) reported Q4 2025 results today with record annual sales of $23.5 billion but disappointed on profitability. While revenue beat consensus by 0.6%, adjusted EPS of $3.40 missed the Street's $3.89 estimate by 12.6%. The stock fell approximately 5.5% in after-hours trading as investors weighed strong top-line momentum against margin compression and a significant free cash flow shortfall.

The quarter capped a transformative year for WESCO, with organic sales growth accelerating each quarter—from 6% in Q1 to 9% in Q4. Data center sales surged over 50% for the full year, reaching approximately $4.3 billion and cementing WESCO's position as a critical infrastructure supplier in the AI buildout.

Did WESCO Beat Earnings?

WESCO delivered mixed results against consensus expectations:

The EPS miss reflects continued margin pressure from project and product mix, particularly in the Communications & Security Solutions (CSS) segment where large data center projects carry lower gross margins but higher asset velocity.

Full-year 2025 adjusted EPS of $12.91 came in below the company's prior guidance range of $13.10-$13.60, primarily due to weaker-than-expected Q4 profitability.

What Did Management Guide for 2026?

WESCO initiated 2026 guidance with expectations for continued growth acceleration:

The guidance midpoint implies approximately 20% EPS growth, driven by operating leverage and margin improvement as the company laps elevated working capital investments. Management noted January sales per workday were up approximately 15%, signaling strong momentum entering 2026.

How Did the Stock React?

WCC shares fell approximately 5.5% in after-hours trading following the release:

The negative reaction likely reflects:

- EPS miss magnitude — 12.6% shortfall versus consensus

- FY2025 free cash flow disappointment — Only $54 million versus $400-$500M guidance

- Margin concerns — EBITDA margin compression despite strong sales growth

However, the strong 2026 outlook and record backlog (+19% YoY) may provide support as investors digest the results.

What Changed From Last Quarter?

Several key trends evolved from Q3 2025:

Improvements:

- UBS returned to consecutive growth — Second straight quarter of positive organic sales (+3.1%), driven by investor-owned utilities

- Backlog hit all-time record — Up 19% YoY with CSS backlog surging ~40%

- EES maintained momentum — Organic sales +8.8%, construction up mid-teens on infrastructure projects

Concerns:

- Free cash flow collapse — FY2025 FCF of just $54 million vs. $400-$500M guidance

- Working capital investment — Net working capital increased to 20.1% of sales as inventory and receivables grew to support accelerating demand

- Public power still soft — Continued destocking impacts margin, though recovery expected in 2026

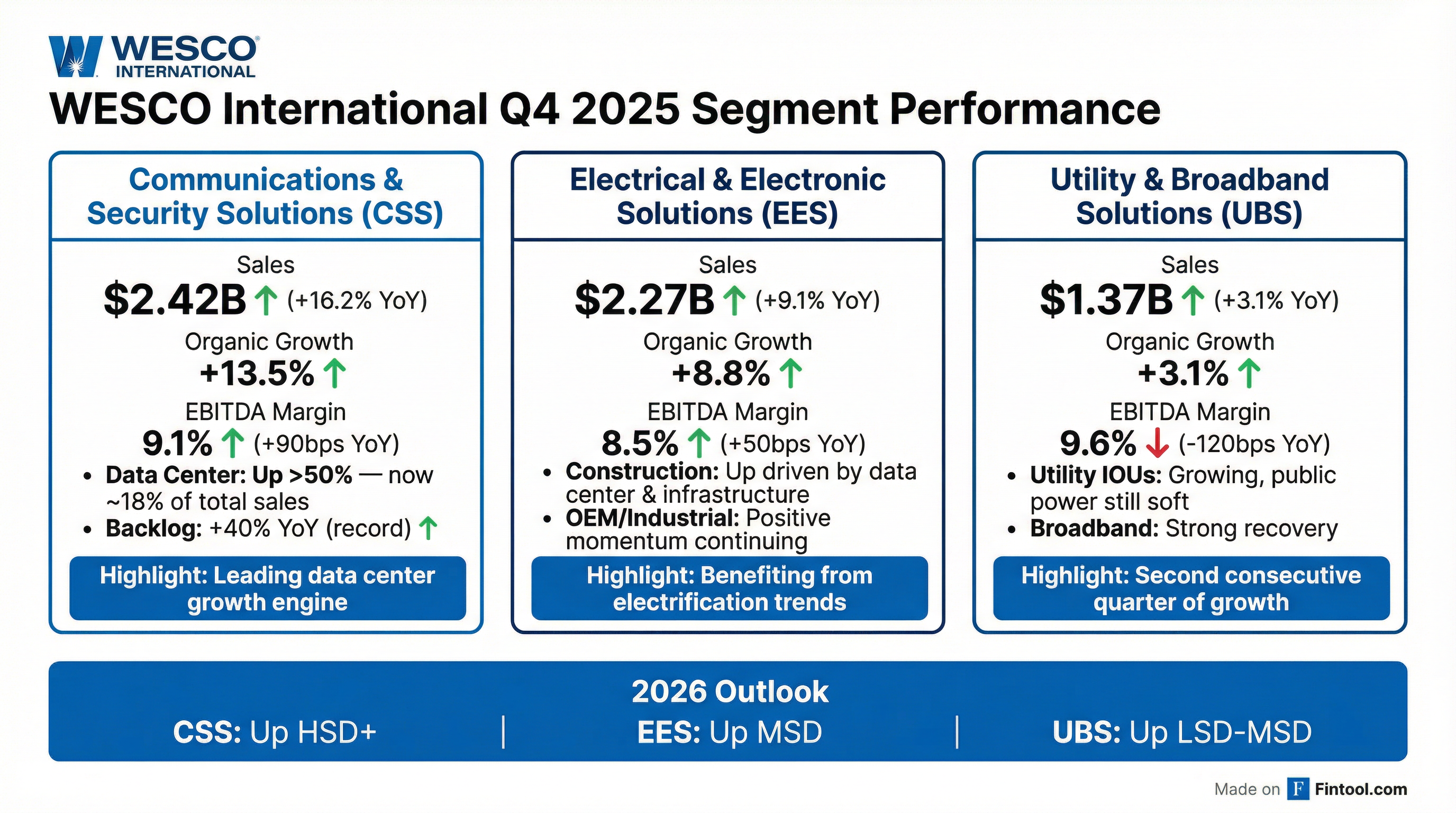

Segment Performance: Data Center Engine Keeps Firing

Communications & Security Solutions (CSS) — 39% of Sales

CSS remained the growth engine with 16.2% reported sales growth and 13.5% organic growth. Data center sales drove the outperformance, with hyperscale and multi-tenant customers continuing to expand capacity for AI workloads.

For 2026, CSS is expected to deliver high-single-digit-plus growth, with data center solutions continuing to lead.

Electrical & Electronic Solutions (EES) — 38% of Sales

EES delivered 9.1% reported and 8.8% organic growth, benefiting from construction activity (data centers, infrastructure) and OEM strength.

EES is expected to grow mid-single-digits in 2026 with contributions from construction, industrial, and OEM.

Utility & Broadband Solutions (UBS) — 23% of Sales

UBS returned to growth for the second consecutive quarter (+3.1% organic), driven by investor-owned utilities while public power remained challenged.

Margin compression reflects competitive pressure in public power markets. For 2026, UBS is expected to grow low-to-mid-single digits as utility demand recovers.

The Data Center Story: Why It Matters

WESCO's data center business hit approximately $4.3 billion in FY2025, representing 18% of total company sales and growing over 50% year-over-year. This positions WESCO as a critical infrastructure supplier for the AI buildout, spanning both:

- White space (~80% of data center sales via CSS): IT infrastructure, racks, cabling, security systems

- Gray space (~20% via EES): Power distribution, electrical infrastructure, cooling systems

The company provides "holistic power-to-compute solutions" across the data center lifecycle, from power delivery through to rack and equipment installation.

Record backlog (+19% YoY overall, +40% in CSS) provides visibility into continued growth, though investors should monitor margin trajectory as large hyperscale projects can pressure gross margins.

Free Cash Flow: The Elephant in the Room

FY2025 free cash flow of just $54 million was the quarter's biggest disappointment, missing the $400-$500 million guidance by a wide margin.

The shortfall reflects heavy investment in working capital to support rapid sales growth:

Management guided to $500-$800 million free cash flow for 2026, implying a significant recovery as working capital intensity normalizes with more stable growth rates.

Key Risks and Watch Items

- Margin sustainability — Data center project mix continues to pressure gross margins; company targeting 20-30 bps annual EBITDA margin improvement

- Working capital efficiency — FCF conversion must improve from FY2025's ~8% of adjusted net income

- Public power recovery — UBS margins depend on destocking ending in 2026

- Leverage — Financial leverage ratio increased to 3.4x from 2.9x YoY due to debt-funded growth

The Bottom Line

WESCO delivered record sales growth but disappointed on profitability, reflecting the trade-off between capturing data center demand and preserving margins. The 12.6% EPS miss and free cash flow shortfall drove after-hours weakness, but the strong 2026 outlook (+20% EPS growth at midpoint) and record backlog suggest the fundamental growth story remains intact.

Investors should watch for:

- Q1 2026 margin trajectory as management targets sequential improvement

- Free cash flow conversion improvement toward the $500-$800M guidance

- Data center order momentum as AI infrastructure spending continues